As a trusted advisor to wealthy individuals and families, the “family office” plays a primary role in identifying and assessing opportunities for wealth generation and perpetuation. The scope of its responsibilities spans traditional wealth management, to include tax planning, philanthropic giving and risk management.

Given the nature of the advice and the inherent risk exposure associated with financial consulting and transaction execution, it is essential that family office managers perform an internal evaluation of the business and legal risk associated with client engagements.

To that end, there are a number of prudent questions for the staff of a family office to ask themselves prior to taking on a client:

- What is the family office’s risk appetite and what potential factors might influence that appetite?

- What are the key risks facing the family office?

- What potential risks will severely affect operations and financial success; are these risks correlated?

- What applied risk-management strategies will the office employ to reduce volatility and lower exposure and cost?

- Do existing risk-mitigation strategies provide reasonable protection against “catastrophic” events from an operational, reputational and cash-flow perspective?

Both parties –the family office and the family– should be asking questions of each other to minimize exposures on both sides.

The other side of the coin is, of course, the protection of the clients. As families become more comfortable relying on their family office to manage a number of administrative and financial functions for them, assumptions may be made and risks overlooked. It is imperative that the family office staff, as part of the discovery process, continue to ask a number of questions of their clients:

- What are the key exposures faced by the family? How are they measured and mitigated?

- What is the family’s risk tolerance in terms of the loss of a key family member, assets, liquidity or reputation?

- Will the introduction of a “family” risk management strategy allow the family to assume new risks or expand current activities?

- How can insurance become a useful tool in protecting the family and reducing overall risk volatility?

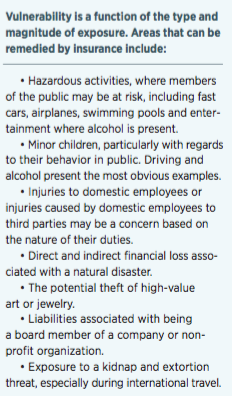

The process of evaluating the purchase of personal insurance begins with an assessment of an individual’s net worth and vulnerability in terms of exposure. An evaluation of net worth should also look at the liquidity and concentration of assets and the cost of capital associated with borrowing funds to replace items affected by an insurable event or lawsuit. This analysis will inform an individual’s risk appetite and pain threshold.

Perhaps the most important aspect of the relationship between a family office and a family is the issue of communication. As a family’s interests and situations evolve, both parties—the family office and the family— should be asking questions of each other, to minimize exposures on both sides. This constant communication will ultimately limit stress and build trust.

This article was originally published in the August/September 2016 issue of Worth.