The hedge fund industry has gone through seismic change due to institutionalization starting at the turn of the century.

It’s hard to remember, but before the tech meltdown of the early ’00s, hedge fund investing was dominated by high net worth individuals and family offices. About 20 percent of hedge fund assets came from institutional investors like pension and sovereign wealth funds, endowments, foundations and funds of funds. But in the past decade, the sources of hedge fund money have changed dramatically. As hedge fund assets have grown from $1.6 trillion in 2009 to $3.2 trillion in 2018, according to BarclayHedge, the percentage of institutional money has surged. Sandy Kaul, global head of business advisory services at Citi, says over two-thirds of that $3.2 trillion now belong to institutional investors.

Institutionalization has produced greater disclosure and discipline. But for a large segment of the industry, this change has significantly altered fund mandates. “Several decades ago, the majority of funds were largely characterized by an aggressive search for performance,” recalls Jon Hansen, managing director at the investment firm Cambridge Associates. “Since [and because of] the financial crisis, there’s been increased emphasis on more risk-averse asset management that prizes consistency and capital preservation.”

This shift largely explains why the vast majority of funds have trailed the market over the past 10 years. Poor investing also hasn’t helped matters.

But in slighting funds’ protracted underperformance since the financial crisis, many industry observers are conflating the monolithic, swashbuckling vision of managers past, who were willing to make outsized bets on the British pound or distressed bank or sovereign debt, with the majority of today’s managers, who instead are providing various strategy exposures to help investors diversify away from long-equity books.

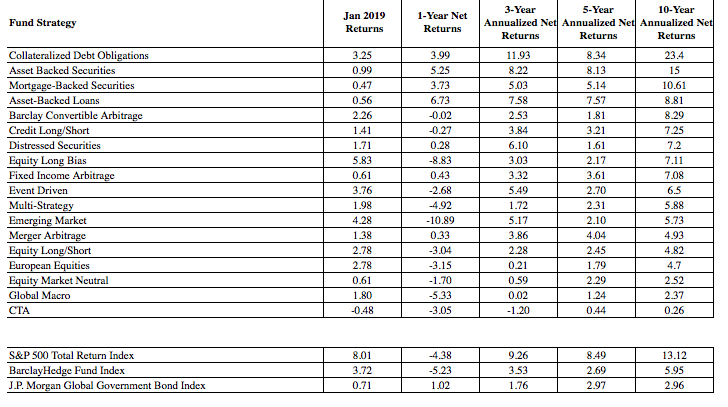

According to BarclayHedge, 16 of the 18 leading strategy categories lagged the market’s 13.12 percent annualized returns over the last 10 years through 2018. And over the past five years, all trailed the S&P 500’s total annual returns of 8.49 percent, with more than half these strategies having earned less than 3 percent a year over this time.

Feeling challenged by the new normal since the financial crisis, many managers have opted for more defensive postures that have collided with external variables, including accommodative central bank policies. They’ve been fueling steady stock and bond rallies, without serious correction, and reducing equity and debt-market volatility. The VIX in 2017 saw record low volatility, nearly half its historical average.

Then came 2018 and the return of volatility, for which many managers had been clamoring. The majority of strategies did outperform the market, which lost 4.4 percent. But when tallying the average return of each individual fund, the industry still trailed the S&P 500 by 75 basis points.

BarclayHedge Indices and Averages Ending December 2018

Many managers could certainly be doing a better job. And this is taking a toll on the number of active funds, which, according to Preqin, declined for the first time in 2018 since the financial crisis as liquidations exceeded launches. At the same time, the steady rise in hedge fund allocations slowed in 2018. For some allocators, the hedge fund industry argument for diversification and uncorrelated market returns haven’t been enough, especially when managers are collecting healthy fees while passive stock exposure continues to rally and an increasing number of ETFs are providing inexpensive market hedges.

“It’s our belief,” says Cambridge Associates’ Hansen, “that only a very small number of funds offer the kind of risk-adjusted returns that justify inclusion in most portfolios.”

But that doesn’t mean allocators should think of hedge funds as some bygone investment relic that largely provides fund managers a living. Hansen believes the right hedge funds can play an essential role to help balance and smooth portfolio performance over the long run.

One dramatic example: the $1.4 billion AlphaQuest Original systematic macro strategy. Over the last 10 years through 2018, it has generated annualized net gains of 3.67 percent, exceeding global macro and systematic CTA returns, though still well behind the market’s 13.12 percent. But due to extraordinary outperformance during the tech crash and the financial crisis, the strategy has doubled the returns of the S&P 500 since its launch in 1999.

“AQO’s returns over the last two decades,” explains Rick Weeks, chief investment officer of $1.4 billion advisory VWG Wealth Management, who has clients’ and his own money in the fund, suggests “long-term performance is more geared to how assets perform during market shocks than how they fare during long-term run-ups.”

OPPORTUNITIES

Despite what the industry’s broad numbers are saying, basic screening reveals a host of really good managers that have been excelling across a variety of strategies for many years with moderate volatility and limited drawdown. They’ve responded to the challenges of major government intervention, crowded trades and limited dispersion of returns in a way that collectively speaks to the promise of hedge funds.

Common traits of successful managers: They are experienced, astute observers of markets and investor behavior, contrarian by nature, willing to stick to their convictions and they manage shops whose operations and investor base support their style of investment.

Another common feature is the size of the fund.

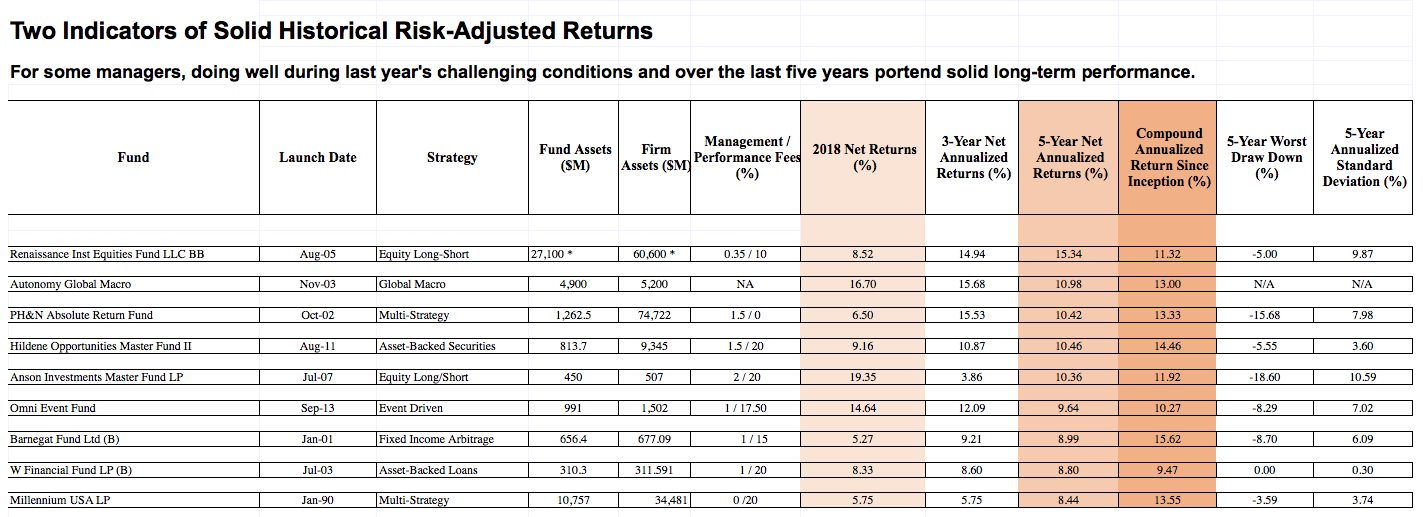

There are very good large funds that have delivered solid returns over many years, including Renaissance, Citadel and Autonomy. Being smaller can also be an asset. Hunting in the sub-billion-dollar space can turn up unexpected quality, with solid operational structure, because it can be easier for these managers to excel in tracking a much wider universe of smaller investments.

In comanaging the $450 million hedged equity Anson Investments Master Fund, Amin Nathoo explains, “we are able to more quickly respond and profit from opportunities across all segments of the market than much larger funds that can’t establish sufficient exposure in smaller-cap shares.” Anson massively outpaced last year’s down market, returning more than 19 percent. And since the fund’s launch in July 2007, it’s racked up net annualized gains of 11.8 percent. Even more telling, the last three annual Barron’s 100 hedge fund surveys were topped by foreign-based funds with an average asset size of $543 million.

Citi’s Sandy Kaul has observed rising family office interest in sub-$500 million shops, building general partnership stakes of up to 25 percent along with limited partnership exposure. “They are likely establishing these dual positions to tap into both sides of the hedge fund business,” explains Kaul, “as well as to get a break on LP fees.”

Panayiotis Lambropoulos, a hedge fund portfolio manager at the $28 billion Employees Retirement System of Texas, believes “in the merit of proven, smaller, institutional-caliber managers to help potentially achieve long-term investment goals.” ERS has started a joint venture with PAAMCO Prisma to develop a “farm system” of emerging managers, aiming for initial exposure of $250 million to $500 million in several emerging managers over the next three years.

“We’re hoping these managers will not only help enhance our performance through their current fund returns but by developing new, distinct investment vehicles,” explains Lambropoulos.

In the structured credit space, the $814 million Hildene Opportunities Fund II, comanaged by Brett Jefferson and Dushyant Mehra, was up more than 9 percent last year and nearly 15 percent annually since its inception in August 2011. And it’s achieved this with minimal volatility and drawdown (both figures around 5 percent).

Hildene targets value in domestically focused high-yield credits of regional and community banks and financials, corporate debt, real estate, and consumer and mortgage debt. “Their complexity can give an edge to investors who can drill down and truly distinguish risk and opportunity,” explains Mehra. This is especially true for smaller segments of structured credits, which larger firms avoid because there isn’t sufficient scale to meet their needs.

The fund has achieved consistent performance by staying relatively small, applying hedges, seeking high current yield as ballast and being quick to adjust duration when structured credit markets change. When there haven’t been sufficient opportunities, the fund has periodically closed to new investors and has returned over $150 million in capital.

Another unique feature: Half the fund’s performance fees are not paid to the manager until investors redeem. After the financial crisis, Jefferson heard investor concerns about funds doing well one year, crystalizing hefty performance fees, then collapsing the next. He believes “deferring a portion of incentive fees better aligns us with what our investors are looking for: attractive long-term risk-adjusted returns.”

One of the more unusual fixed-income relative value funds is Bob Treue’s $656 million Barnegat fund, which has racked up annualized returns of 15.62 percent since he started up in January 2001. Like Hildene, he’ll tell investors when he can’t accept money because he doesn’t see sufficient opportunities in which to deploy it. And he’s remarkably upfront about his fund’s caveats, sending an eight-point brief to all prospective investors. This includes admission that he has no ceilings or floors in using leverage, he doesn’t employ strict stop-loss rules and redemption is done incrementally across nine months.

In taking the long view that rationality will ultimately close gaps between securities that should be trading in sync, Treue maintains a large amount of unencumbered cash to meet margin calls and to enable him to add to down positions. And his stable investor base understands the process.

A current investment example: In early March 30-Year UK Gilts were yielding 1.71 percent while an equivalently-termed inflation swap was at 3.52 percent. “Treasurys should always pay more than inflation swaps,” says Treue.

Gregg Winter’s $313 million W Financial fund shows diversification is not always essential for solid, steady performance.

Launching his shop in July 2003, Winter saw a low-risk opportunity in timely lending of first-lien bridge loans to qualified borrowers with quality New York City properties, which banks were unable to address.

By lending amounts well below a property’s market value and with loans being typically no longer than one year in duration, the fund has chalked up annualized returns of 9.45 percent, with virtually no volatility or drawdown. And last year was pretty much the same with the fund up 8.33 percent.

LOOKING BEYOND

With the turbulence of last year’s fourth quarter not far in the review mirror compounded by today’s inverted yield curve, which may portend recession, hedge funds’ defensive posture may start paying off.

Marc Sbeghen, head of hedge fund research at the Geneva-based Iteram Capital, says the firm is becoming more risk-averse. It recommends reducing investments in directional strategies involving event-driven and hedged-equity exposure and to increase exposure to more global macro, equity-market-neutral, credit long-short and fixed-income arbitrage strategies.

In considering a similar pivot, Texas ERS’ Lambropoulos sees two systemic concerns. “We first saw how fear of geopolitical along with debt and equity-market risks got quickly translated into a massive sell-off with remarkable velocity during last year’s fourth quarter,” Lambropoulos says. “This year we saw concerns about the U.S. consumer manifested by the immediate effects of the government shutdown. All this suggests greater vulnerability of retail-oriented loan and housing markets than most of us realized.”

Many market observers believe the underlying strength of the U.S. economy and markets will endure for a while longer. CA’s Jon Hansen thinks 2018’s fourth quarter turbulence was largely technically driven, rather than reflective of systemic threats to the present corporate and economic growth.

But Lambropoulos is more skeptical, believing broad market dynamics have broken down. “We’ve seen an explosion of debt issuance and stretched equity valuations along with plenty of events to move prices, but a surprising lack of dispersion among assets,” he notes.

There are a lot of things that worry Autonomy Capital’s Robert Gibbins. “Impact of the U.S. tax breaks will likely peter out after June, Chinese growth will slow as the country continues to deleverage and Europe will continue to be weighed down by structural issues it fails to resolve,” Gibbins says.

This didn’t inhibit Gibbin’s $4.8 billion global macro fund from racking up tidy gains of nearly 17 percent last year (more than 13 percent annualized since he launched in 2003). But these issues suggest a more challenging investment environment going forward.

His most compelling long-term idea? Continuing reforms in Argentina over the next decade could make the country a huge long-term out-performer.

But Gibbins is unnerved by one risk: climate change. He fears the likely failure to effectively address increasingly destructive weather will fuel higher risk premiums across asset classes, which markets are not considering.

The takeaway from this industry walkabout: skillful diversification with disciplined, seasoned managers, large or small, who have proven their ability to read markets well and invest shrewdly regardless of what stocks and bonds are doing will serve investors well. But persistent monitoring is essential, since past performance is just that.

Eric Uhlfelder created and wrote the “Financial Times Hedge Fund Review” for four years and managed Barron’s “Top 100 Hedge Fund Survey” for the last 11 years. Upon the advent of the euro, he authored the book Investing in the New Europe (Bloomberg Press, 2001).