In “Fear of Crashing” investor, author and philanthropist Peter Lynch considers the potential of a market correction in September 1995, and, along with financial writer John Rothchild, he advises how to prepare for, react to and recover from such uncertainty.

The Dow’s passing 4700 has brought new worries about a nasty correction. The worrying started as soon as we recovered from the last nasty correction, in 1990. There’s no end to the list of probable causes for a repeat: Too many mutual funds are chasing too few stocks, stocks are overpriced, the dividend yield on the Dow is at an all-time low, and—this one is my favorite—not enough investors are worried.

Let me go on record with Lynch’s prediction: Another big correction is on the way. I’d bet the ranch on it, if I had a ranch. It may come this year, next year, or the year the Red Sox win the World Series (don’t hold your breath!); but sooner or later, it will happen. You read it here first.

On what do I base this bold assertion? Stocks have declined 10 percent or more on 53 occasions since the turn of the century. That’s roughly one correction occurring every two years.* And on 15 of these 53 occasions, stocks have declined 25 percent or more. That’s one nasty correction (also known as a bear market) every six years.

For all I know, another bear may have arrived on the scene by the time this article reaches the newsstands. Or the equity gods may wait until the Dow reaches 6500 before they decide to knock it back to 4700, today’s highs becoming tomorrow’s lows. Or we could drop from today’s levels straight down to 3100.

Make no mistake: Corrections can be scary experiences. People lose confidence in the economy, in their portfolios and in the companies in which they’ve invested. It’s like a storm that rolls in and blackens the sky. Fear sets in.

Most stocks fluctuate 50 percent from top to bottom every year, without any fanfare.

If only we didn’t have indexes—the Dow, the Standard & Poor’s 500, and so forth—that enable us to track the ups and downs of “the market,” we’d never have this problem with corrections. Do you know what the range is between the high and the low price of the average stock on the New York Stock Exchange in any given year? Fifty percent. So most stocks fluctuate 50 percent from top to bottom every year, without any fanfare.

We remember the 1000-point drop in the Dow from August to October 1987, the scariest correction in recent times. But we forget the 1000-point rise in the Dow in the 11 months preceding that drop—a remarkably fast gain, considering that it had taken the Dow four years to tack on the previous 1000 points. If we had been sequestered like a jury during all of 1987, we would have come out thinking the market was flat for the year, and nobody would have panicked.

But we do have indexes and we are preoccupied with their ups and downs, so we will have scary corrections. If we tack on another 1000 points from here and the Dow rises to 5700 in short order, the chances of another big decline increase considerably.

Assuming you agree with my forecast, how can we prepare? Mostly by doing nothing.

This is where a market calamity is different from a meteorological calamity. Since we’ve learned to take action to protect ourselves from snowstorms and hurricanes, it’s only natural that we would try to prepare ourselves for corrections, even though this is one case where being prepared like a Boy Scout can be ruinous. Far more money has been lost by investors preparing for corrections or trying to anticipate corrections than has been lost in corrections themselves.

The first mistake is hedging the portfolio. Anticipating a drop in the market, the skittish investor begins to dabble in futures and options, the kind of investment that will make a profit when stocks decline. People think of this as correction insurance. It seems cheap at first, but the options expire every couple of months, and if stocks don’t go down on schedule, people have to buy more options to renew the policy. Suddenly, investing isn’t so simple. Investors can’t decide whether they’re rooting for stocks to falter, so their insurance will pay off, or for a rally, for the sake of the portfolio.

Hedging is a tricky business even the pros haven’t mastered—otherwise, why have so many hedge funds gone out of business in recent years? Hedge-fund managers have been sighted in unemployment lines.

The second and more prevalent mistake is the ritual known as lightening up. This time, our skittish investors, again fearing the correction is imminent, sell some or all of their stocks and stock mutual funds. Or they put off buying stocks in companies they like and sit on their cash, waiting for the crash. “Better safe than sorry,” they tell themselves. “I’ll wait for the day of reckoning, when all the suckers who didn’t see this coming are wailing and gnashing their teeth, and I’ll snap up bargains left and right.” (But once the market reaches bottom, the cash sitters are likely to continue to sit on their cash. They’re waiting for further declines that never come, and they miss there bound.)

They may still call themselves long-term investors, but they’re not. They’ve turned themselves into market timers, and unless their timing is very good, the market will run away from them.

Market timing was quite popular about 2700 Dow points ago, when clients of mutual funds were encouraged to switch back and forth from stock funds to the money market, thereby avoiding any unpleasant corrections. The signals were sent out by self-appointed heads of “switching services” who charged hefty fees (as high as 3 percent a year) for their canny advice. People were paying their switch-fund advisors two to eight times as much as they paid in management fees to the funds themselves.

Whereas in most states barbers have to pass a test before they are allowed to cut hair, there is no test for switch forecasters. My advice for anyone who is still paying for such a service: Go back and carefully check the results before you give another penny to a switching service. Have you really avoided the corrections, or have you avoided the best months of the greatest bull market in history? It pains me to think how many people have done the latter.

A review of the S&P 500 going back to 1954 shows how expensive it is to be out of stocks during the short stretches when they make their biggest jumps. If you kept all your money in stocks throughout these 40 years, your annual return on investment was11.4 percent. If you were out of stocks for the ten most profitable months, your return dropped to 8.3 percent. If you missed the20 most profitable months, your return was 6.1 percent; the 40 most profitable, and you made only 2.7 percent. Imagine that:If you were out of stocks for 40 key months in 40 years, trying to avoid corrections, your stock portfolio underperformed your savings account.

The same computer that gave us that revelation also contributed the following: If you invested $2,000 in the S&P 500 on January1 of every year since 1965, your annual return has been 11 percent. If you were unlucky and managed to invest that $2,000 at the peak of the market in each year, your annual return has been 10.6 percent.

Or if you were lucky and invested the $2,000 at the low point in the market, you ended up with 11.7 percent. In other words, in the long run it doesn’t matter much whether your timing is good or bad. What matters is that you stay invested in stocks.

Whether your timing is good or bad. What matters is that you stay invested in stocks.

Recently, Forbes published its hit parade of the richest people in the world, and I was reminded that there’s never been a market timer on the list. If it were truly possible to predict corrections, you’d think somebody would have made billions by doing it.

The fact that nobody has done so ought to tell us something about our chances of dodging the drops. Warren Buffett weighs in at No. 2 on the Forbes list. He got there by picking stocks and not by switching in and out of them.

Buffett switched only once in his career, in the late 1960s, when Wall Street fell so hopelessly in love with a select group of growth companies that no price was too high to pay for them. At the point of maximum silliness, McDonald’s was selling for 83 times earnings and Disney for 76; whereas in saner times, they might sell for 20 times earnings. These two companies, and 48 others in the so-called Nifty Fifty, were so overvalued that it took them 10 years to catch up to their price tags. So if you’re looking for more concrete advice than I’ve offered so far, take a tip from Warren Buffett and get out of stocks that are selling for 83 times earnings. Otherwise, stay the course and resist the temptation to outsmart corrections.

In telling you this, I’m assuming you’re in stocks for the long haul: two score years or beyond. Never invest money in stocks if you are going to need it for some other purpose in the foreseeable future. Twenty years is a reasonable horizon for investing. That ought to be long enough for your stocks to overcome the worst of times, such as the stretch between 1966 and 1982, when the Dow stumbled from a peak of 1000 to a nadir of 777 And here’s a reassuring point: When you include the dividends, stocks in the S&P 500 gave a total return of 75.37 percent during that depressing 16-year period, or 3.5 percent annualized. Thanks to dividends, corrections aren’t necessarily as bad as they’re made out to be.

As soon as you realize you can afford to wait out any correction, the calamity also becomes an opportunity to pick up bargains.

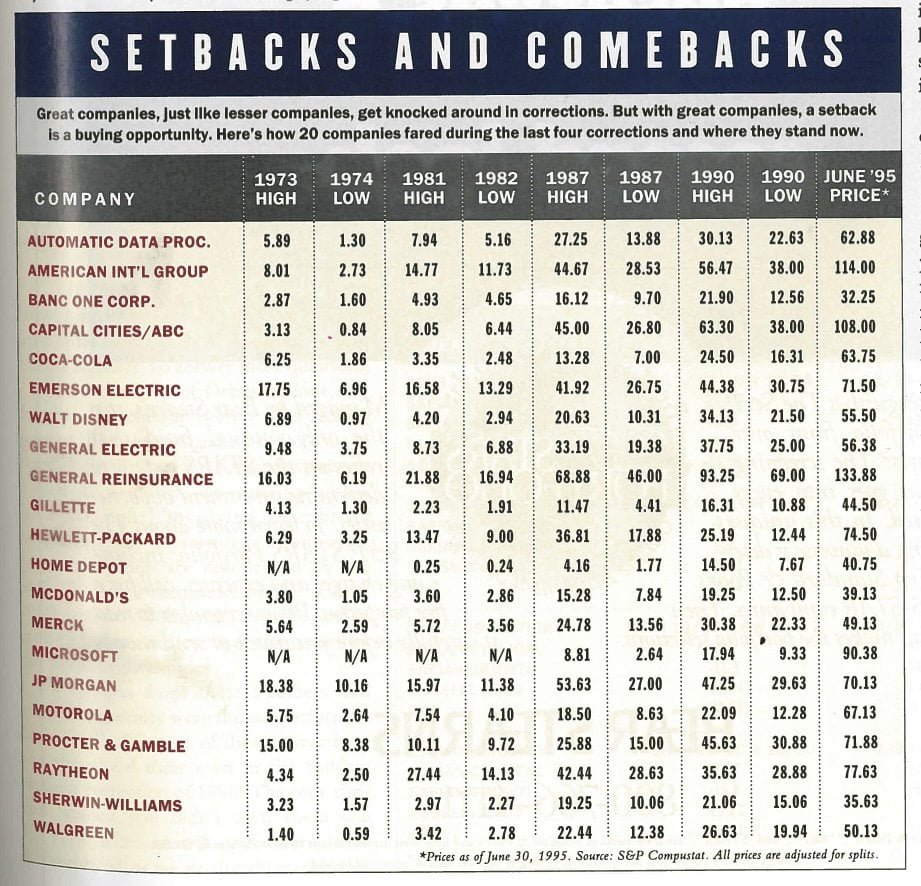

This table (below) shows a few examples of how the four nastiest corrections in recent history (1973-74, 1981-82, 1987, and 1990) actually paid us a favor by giving us the chance to buy great companies at fire-sale prices. If it’s happened before, it will happen again.

THE ANATOMY OF A CORRECTION

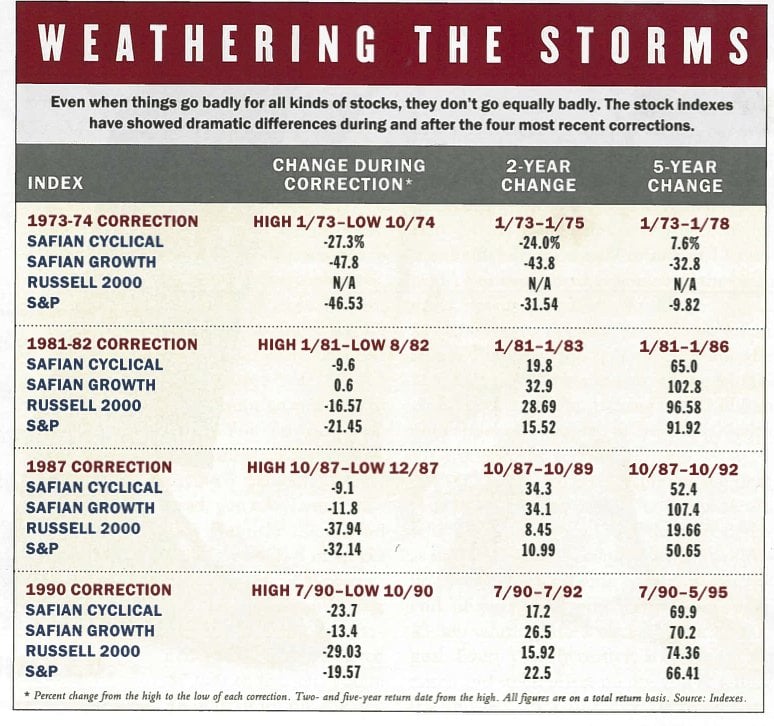

How have different types of companies fared in those four corrections? Do all stocks correct equally? To answer those questions, I enlisted the help of Deborah Pont, my dogged researcher at Worth, who in turn enlisted the help of Standard & Poor’s, the Frank Russell Co., and Safian Investment Research. Together, we came up with a large table (below) involving four broad categories, each represented by an index. Large companies are represented by the S&P 500; small companies by the Russell 2000; growth companies by the Safian growth index; and cyclical companies by the Safian cyclical index.

It’s obvious from these numbers that growth companies were the star performers during and after two of these corrections, and they held their own in the Saddam Hussein correction of 1990.The only time you wished you didn’t own them was 197374, when growth stocks were grossly overpriced, as we’ve already mentioned.

For those who haven’t boned up on the subject, a growth company is a steady performer that can prosper in all economic conditions, as opposed to a cyclical, which lurches from rags to riches and back again. A typical lineup of growth companies includes those that make software and soft drinks, drug makers and fast-food chains, specialty retailers and service-related businesses, and even a cigarette manufacturer, Philip Morris. Sam Stovall, editor of Standard & Poor’s Industry Reports and an avid student of corrections, calls these the “eat ’em, drink ’em, smoke ’em, and pay-for-it-by-going-to-the-doctor type stocks.”

After the infamous 1987 bear market, when investors in the Dow industrial stocks were traumatized by a 33 percent loss from the August top to the October bottom, including the terrifying 508-point one-day drop, investors in growth stocks were still ahead by 8.5 percent and getting a good night’s sleep. In 1990, growth stocks lost a bit more ground than the cyclicals on the downside but far less than the three other categories of stocks, and they’ve kept pace with the cyclicals on the upside.

I’ve long been a fan of growth companies, but in the course of collecting data for this article, I was amazed to discover that since 1949, an investment in the 50 growth stocks on Safian’s list has returned over 230-fold, while the cyclicals have returned only 19-fold. Whether they are owned individually or as an elementof mutual funds, growth stocks have given their owners fewer heartaches and many happy returns.

THE CASE FOR ZERO PERCENT BONDS—THAT IS, YOU SHOULDN’T OWN ANY

This brings me to an investment strategy I described in my second book, Beating the Street. If I convince you of its merits, you will never again buy a bond or a bond fund, and you’ll stay fully invested in stocks forever.

There are two main arguments for owning bonds: They give you income so you can pay the bills, and they add ballast to your portfolio. Unless you’re talking about bonds of the short-term variety (two to four years), the ballast argument is false. Long-term bonds can be almost as volatile as stocks. They have their own corrections: When interest rates go up, bond prices go down just as fast as stock prices. If you’re not willing to hold a bond to maturity, you’re exposing yourself to potential losses, the same as in stocks. And bonds have no upside to reward you for this risk if they’re held to maturity. You collect the interest along the way, but in the end, the best you can hope for is to get reimbursed.

In the nine decades in this century, bonds have outperformed stocks only once—in the 1930s. They came close in the 1980s, but in the first half of the 1990s, stocks have once again proved their superiority. People are living longer these days, so many retirees who buy bonds for the income are discovering that they may end up needing more money than they thought they would. They could use some growth in their principal, but they aren’t getting it.

The strategy I’m proposing can offer the best of both worlds: money to live on that normally comes from bonds and growth that comes from stocks. Here’s how it works. You sink 100 percent of your investment capital into a portfolio of companies that pay regular dividends. You could do this the easy way and invest in an S&P 500 index fund, currently yielding about 3 percent. Or you could select a few “dividend achievers,” as identified by Moody’s. These are the companies that have a habit of raising their dividends year after year no matter what.

According to the latest Moody’s list, no fewer than 332 publicly traded companies have accomplished this for at least 10 years in a row. The list includes some obscure names but also a lot of familiar ones, the likes of Wal-Mart, Hasbro, Philip Morris, and Merck.

Since dividends are paid out of earnings, these dividend achievers couldn’t have compiled such a record without having enjoyed consistent success in their core business, whatever it is. So you’re looking at a group of profitable enterprises with staying power.

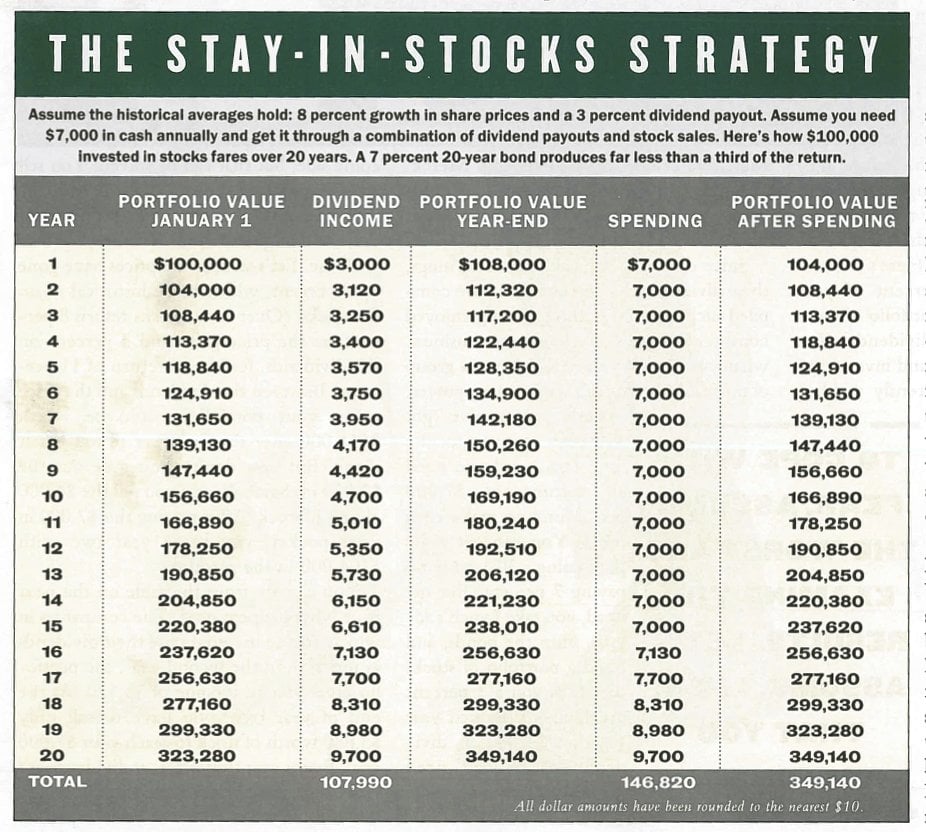

Let’s say you’ve got $100,000 to invest for the long term, and you need an income of $7,000 per annum to make ends meet. You can get it by purchasing a 30-year bond paying 7 percent. But instead, you take Lynch’s advice, shun the bonds, and build a portfolio of stocks that pays you a 3 percent dividend. In the first year you get $3,000 in dividends. Since you need $7,000to live on, you’re $4,000 short on the income side, but that can be solved. You sell $4,000 worth of stock.

It may sound crazy to be selling shares that you bought 12 months earlier, but bear with me. Let’s assume the prices have gone up 8 percent, which is the historical norm for stocks. (Overtime, stocks return 8 percent on the price gains and 3 percent on the dividends, for a total return of 11 percent.) Between the dividends and the price gains, your portfolio would be worth$111,000 after the first year if you left it alone. But you don’t. You take out the $3,000 in dividends, and you sell the $4,000 chunk of stock. After putting this $7,000 in your pocket, you begin year two with $104,000 in the account.

You can see from this table (below) what happens next. The companies in which you’ve invested raise their dividends as usual, so in the second year, the portfolio gives you an income of $3,120. At the end of year two, you have to sell only $3,880 worth of stock to reach your $7,000 goal. Every year there after, as dividends are raised and stock prices go up, you’re selling less and less stock to cover your expenses. In year 16, you receive $7,000 out of the dividends alone, and from this point forward, you never have to sell a single share to get the customary payout. In fact, your payout goes up.

These numbers are theoretical, but they’re based on the average returns from stocks and dividends over this entire century. Assuming these same results hold for the future, after 20 years, you roriginal $100,000 will have grown into $349,140. You’ll be more than three times richer than when you started, on top of the $146,820 worth of dividends you’ve spent along the way. By taking the bond route, you would have received $140,000 in interest and gotten your $100,000 back.

If this dividend strategy is such a great idea, why aren’t more people taking advantage of it? I suspect it’s the same reason they own more bonds than stocks ($9.4 trillion to $6.5 trillion, at current count) when stocks are clearly more profitable overtime. They think they’re jinxed. They’re worried about the next nasty correction, and they’re convinced it will happen the day after they invest in stocks. Perhaps you count yourself as one of this unlucky crowd.

The whole country can be unlucky, and stocks will still do better than bonds over 20 years.

The best way to cope with the fear of crashing is to assume the worst and examine the results. Let’s assume, then, that you are jinxed, and the day after you invest your entire $100,000in dividend achievers, the market has its worst session in history and your portfolio loses 25 percent of its value overnight.

Fidelity’s Bob Beckwitt ran the numbers. In spite of the immediate25 percent loss, if you stuck with the plan, sold shares to augment the return, and collected your $146,820 in dividends along the way, at the end of the 20th year your portfolio would be worth$185,350. That’s not as good as $349,140, but it puts you $85,350ahead of the $100,000 bond.

Let’s imagine an even more terrible case: a recession that lasts20 years. The country is in its worst slump since the Great Depression. In this prolonged crisis, companies struggle to increase their profits, and instead of share prices and dividends increasing at the normal rate of 8 percent and 3 percent, respectively, these returns are cut in half. Still, if you stuck with the program and removed $7,000 from the account each year, you’d end up witha $100,000 portfolio—exactly the same as getting your principal back from a bond.

Again, these calculations are theoretical, but the results are so favorable to stocks that there’s a lot of room for error. Everybody can be unlucky, the whole country can be unlucky, and stocks will still do better than bonds—assuming you keep your money in stocks for 20 years or longer. This is where male retirees will say: “I don’t have 20 years to wait, because I’m 65 already and my life expectancy is 68.2. I only have 3.2 years to live.”

In fact, if a man gets to 65, he’s likely to make it to 85, and if he and his wife both reach 65, there’s a good chance one of them will make it to 90. People have more time than they think to ride out corrections, which is the main reason we shouldn’t be worried about the next one, or the one after that.

I’ll leave you with the latest gloomy report from Wall Street: Experts say stock prices will collapse because too many people have become long-term investors. The way they see it, the idea of long-term investing is so popular, it has to be wrong. Does that mean the earth really is flat?

Ask yourself: Why do I own these companies?

When a correction hits and people around us are losing their heads, as Kipling would say, we can find reassurance in the following: What makes stocks valuable in the long run isn’t “the market.” It’s the profitability of the shares in the companies you own. As corporate profits increase, corporations become more valuable, and sooner or later, their shares will sell for a higher price. Historically, corporate profits have advanced by 8 percent a year. This 8 percent, along with the 3 percent dividend yield, is what accounts for the 11 percent annual return. There may never have been a year when they had a total return of exactly11 percent, but that’s the average over time. Corrections or no corrections, that’s what stocks produce, because that’s what corporations produce.

Even if corporate profits grew at 6, 5, or 4 percent, stocks would still advance, albeit at this lower rate. Adding in the3 percent for the dividends, you’d get a 9, 8, or 7 percent total return. That’s still a better return than you’d get from bonds in most decades. Ultimately, to be an investor in stocks, you have to believe that American business has a decent future, as well as business worldwide, and that corporations will continue to increase their profits. If you are as convinced of this as I am, then you’ll never panic in a correction. —P.L.

* In spring 1994, we had a stealth correction. The Dow dropped 10 percent from its January 31 high on three separate occasions, managing to recover its losses before the end of the trading day in each instance. Few people took notice, but maybe that’s why 1995 has been such a good market: The semiannual decline has already sneaked past us.

Reprinted from the September 1995 issue of Worth