Chappaqua, New York, lies a scant 35 miles from Times Square, the Crossroads of the World. Yet the town was, and is, a quintessential American small town. Founded by Quakers, it provided an idyllic landscape for my childhood. But, because the town’s kid-friendly entertainment consisted of browsing the toys at the Penny Auntie five-and-dime store, fun was more often of the ride-your bike or explore-the-woods variety.

Except, that is, when Mother—not my mom, but Mother Nature—grew bored. Few things excited me more than hearing the local weatherman advise folks to stock up on milk, bread and batteries (for the transistor radio), as a nor’easter was primed to shoot up the Hudson come evening.

Planted on our back porch at the appointed hour, I would watch the beeches sway against the darkening skies. And, as the scent of ozone signaled the storm’s approach, one question ran through my mind: Would school be canceled the next day?

The next morning, we’d inspect nature’s handiwork. Were trees down? Had the Saw Mill River Parkway flooded? Wrapped safely in the naiveté of youth, I never truly understood the cost of what could be only predicted, tracked and endured but never controlled.

Ironically, today I make my living helping protect people’s lives, livelihoods and living spaces from all manner of natural disasters. Yet, while I consider the myriad ways to mitigate risk for my clients almost daily, I’ve found that most people still think of natural disasters the way I did as a child: as something amazing, even heartbreaking to watch on CNN, but not something that will ever negatively affect them.

Until, of course, it does.

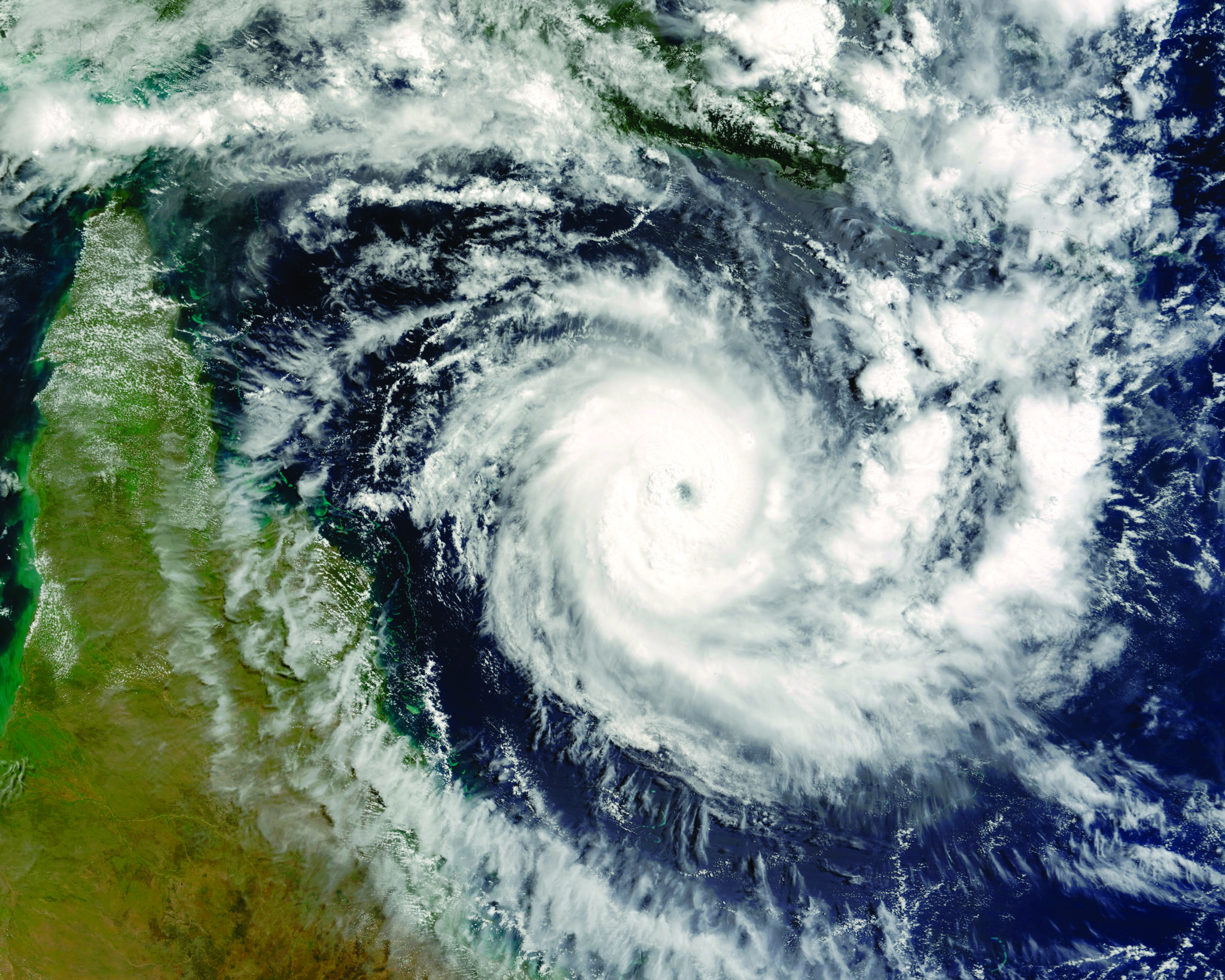

The reality is that many of America’s most disaster-prone areas are often the locations with the most sought-after real estate. Despite a propensity for wildfires, landslides, and, lately, volcanoes in California, Colorado and Hawaii, few homeowners are jettisoning their properties there.

Similarly, on the East Coast, as long as Miami Beach remains above sea level, people will pay into the mid–eight figures for an oceanside penthouse, despite the near certainty of another Andrew or Irma striking in the future.

That’s what insurance is for, correct? It is. But protecting the properties of high net worth families is much more complex than asking how high a deductible they want should a hailstorm damage their roof. Creating a risk-management plan that includes real estate, possessions, investments, assets and potential exposures is a highly complex undertaking.

That’s why today’s leading agents are increasingly turning to big data to determine specific property risk based on the exact location and construction of a home. And, when one considers that many high net worth clients have multiple properties in multiple states, the need for an agent who understands the variances of geographic regions in terms of both potential natural disasters and local building ordinances becomes evident.

A smart agent is as proactive in alleviating risk as in procuring adequate coverage for those times disaster actually strikes. Sometimes, it’s as simple as making sure a property has the proper water shutoff valves installed. Or, it’s specialized work, like bringing in wildfire-mitigation experts or contractors who understand the secrets of building truly earthquake-proof homes.

In other words, an elite agent does more than merely understand policies. He or she researches the intricacies of the risks inherent to a high net worth lifestyle and develops risk-management plans accordingly.

So, the next time “Mother” barges in—uninvited, angry and unpredictable as ever—those who have wisely placed their trust with such agents can rest assured (perhaps not that easily, given the circumstances) that nature’s beautiful fury is a short-term display of power and not a long-term disruption to their lives.