How do we assess the Federal Reserve and recent economic slowdowns?

How do we assess the Federal Reserve and recent economic slowdowns?

As we are studying the cycles of the Federal Reserve’s monetary policy, a most interesting statistic crossed our desk during the holiday season. The average length of time from the last Fed rate hike to the first Fed rate drop was a mere five months. That’s correct: only five short months to the first rate drop. […]

As we are studying the cycles of the Federal Reserve’s monetary policy, a most interesting statistic crossed our desk during the holiday season. The average length of time from the last Fed rate hike to the first Fed rate drop was a mere five months. That’s correct: only five short months to the first rate drop. This statistic made us very uncomfortable with how the Federal Reserve handles monetary policy. Because of the 2008 financial crisis, we have seen more Federal Reserve involvement in the economy in the last few years. The easing and free money from the Fed shows a lot of stimulus coming from an institution whose stated goals are keeping inflation in check and full employment.

How do we assess a Federal Reserve that has low inflation and full employment but still raises rates? The answer is simple: The Fed has modestly strayed from its mandated goals. There are some legitimate reasons for the Fed to raise rates, but most of them involve fixing what the previous Fed chair—from 2014 to 2018—got wrong. It seems that Janet Yellen should have raised rates a little more during her tenure, to bring us back to some level of normalcy. Since neither she nor Ben Bernanke did much to fix the enormous and long-in-the-tooth period of easing monetary policy that they helped create, Chairman Jerome Powell, with a better economy, did it instead. However, it was so late in the cycle that there was no way to actually get back to a normal world, where the Fed was no longer continually stimulating the economy, without causing another problem.

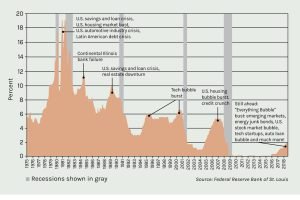

As you can see in the chart above, raising interest rates does cause big problems for the economy going forward. In addition, most Fed watchers would tell you that the Fed contributes most to problems in our economy by overshooting and undershooting in its monetary policy. That is why the most recent action by the Fed is disconcerting. Chairman Powell knows all this history and had the opportunity to chart a new course for the Fed, creating a much softer landing for the economy by not raising rates when inflation allowed him to. At this stage, most investment professionals do not want to see the Fed lower rates because that would translate to real problems, such as a recession or another economic dislocation. The Federal Reserve had all it needed to make this great leap toward changing the outcomes of its own actions, and yet it chose the wrong path once again. Granite Group believes that the Fed should adjust its actions swiftly so a market dislocation does not occur. Powell raised rates at an opportune time in the cycle, but that time has come to an end. The only reason to raise rates from here on would be an unforeseen trend that pushed inflation higher than what we are seeing or predicting. It may be too late at this point to keep the United States from going into a recession, but any more rate increases would all but guarantee that outcome.

Our Federal Reserve is an amazing institution and does great work, but this continued ebb and flow needs to be changed. Members should heed the following words: “The definition of insanity is doing the same thing over and over again and expecting different results.”

The direct byproduct of this growth is our unwavering commitment to the fiduciary promise for our clients, empowering us to build an enduring firm that will serve future generations.

There are generally three places you can give your money—family, charity, or the IRS. The goal of tax planning should be to make sure you give most of it to the first two.

In addition to being entrusted with your most valuable assets, financial advisors are equipped to deploy resources to support philanthropic priorities by recognizing tax-efficient giving strategies, exploring charitable giving vehicles, and identifying opportunities for maximum impact.

As you can see in the chart above, raising interest rates

As you can see in the chart above, raising interest rates