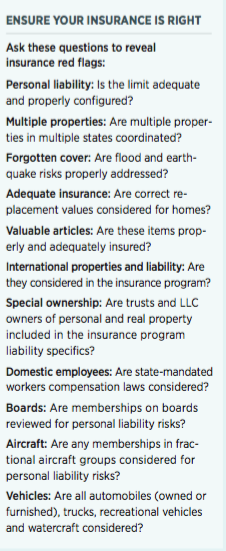

It might sound a bit flippant to say, but you will not know if you need an insurance review until you have one. If your review is like that of most high net worth families, you may buy your insurance one category at a time: home, automobile, watercraft, valuables and excess liability. This approach can create gaps in coverage and loss of package premium discounts.

But even if all the pieces of your insurance puzzle fit neatly together, a property-casualty personal insurance review evaluates three critical measures—competent technical advice, correct pricing and transactional simplicity—of a correctly structured and administered insurance strategy. And in our opinion, for your insurance structure to qualify as high quality, a review should confirm that these five essential components are also in place:

1. A sophisticated underwriter

2. A competent account manager

3. An agency with organizational structure

4. A valid process

5. A trusted advisor

A sophisticated underwriter is an insurance carrier with an adequate credit rating, underwriting capacity, product design, product flexibility, pricing flexibility, claims integrity and ancillary services. Your broker should represent the most sophisticated underwriters, on a national basis. In our case, we represent all five of them.

You will not know if you need an insurance review until you have one.

A competent account manager is an insurance broker with proper technical background and experience. Expert knowledge prevents problems for you. Selecting account managers within the framework of a company’s discipline in operations yields high-quality control.

An agency with organizational structure demonstrates that beyond your account manager, others in the firm are capable of assisting with service and technical questions. You should consider as essential your ability, post-sale, to reach a person knowledgeable about your account whenever you call.

A valid process has adequate incoming information. For example, we use our risk-profile form to capture the salient parts of our conversations. A synthesis of the information results in a written work product for your policies. After you and we review the product, we go to discussion.

A trusted advisor enhances this process by endorsing the concept of the review. If you are among those who feel there is little product differentiation in our field, an advisor plays an important role in demonstrating the subtle differences between adequate and outstanding coverage. The purpose of the insurance review is to make certain yours is the latter and not the former. And if it is not outstanding, the review reveals weaknesses in your coverage that need correcting to make it so.

Insurance services provided through NFP Property & Casualty Insurance, Inc., a subsidiary of NFP Corp. Doing business in California as NFP Property & Casualty Insurance Services, Inc. (Calif. License # 0F15715).

This article was originally published in the August/September 2016 issue of Worth.