In a previous article, my business partner Steve Schwartz discussed non-portfolio-centric ways in which an advisor adds value. I’ll further his points by stating that advisors are worth their weight in gold when they guide clients through temporary bear markets, so that those clients can enjoy the long-standing advances of bull markets.

For that reason, Steve and I both suggest the notion of a “bear market playbook,” not only for the next potential bear market, but for all future bear markets a client investing for a 50-year time horizon can expect to endure.

Expect the Bear Market

Bear markets are painful for clients, regardless of their time horizon. But these markets are even more painful when clients don’t understand that bear markets occur on a frequent basis.

In order to fully enjoy the fruits of the great bull markets, clients must understand that a bear market can and must happen.

Of course, notifying clients that bear markets will occur is very different from predicting bear markets. Notifying clients about these markets merely provides them with a historical perspective. We do not believe that advisors can, or should, suggest that they can predict bear markets with any level of success.

Love the Bear Market

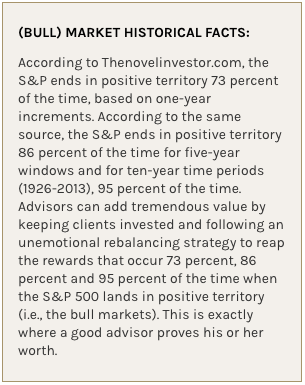

Bear markets should trigger a buying opportunity for any advisor/ client relationship utilizing an asset-allocation strategy, coupled with a rebalancing strategy. If a client started on January 1, 2016, with a diversified portfolio of 90 percent equities and 10 percent fixed income/cash, due to the January market pull-back, the client might actually be closer to 85 percent equities and 15 percent fixed income/cash.

Advisors who guide clients with a strict, unemotional asset allocation and rebalancing strategy will constantly teach clients that short-term corrections are wonderful buying opportunities to purchase equities at a discount.

Understand the Bear Market

Advisors worth their fee are constantly holding the hands of clients and reminding them that bear markets provide volatility. Volatility, in turn, provides a risk premium for equities. That risk premium then provides the real rate of return (inflation-adjusted rate of return) historically found in equities.

Without the volatility and risk premium, equity returns would most likely track the lower-return profile of asset classes that merely track inflation. Genuine advisors should constantly remind clients that bear markets provide needed volatility, which provides the risk premium for inflation above historical returns.

Defend Against the Bear Market

Advisors that lead by planning ahead of portfolio advice will help their clients defend against the bear market by having 6 to 24 months’ worth of their expenses (the burn) in cash or cash equivalents. And, no, cash equivalents are not securities that can be sold and turned into cash!

Expecting, loving, understanding and defending against bear markets, then, inevitably guides an advisor toward communicating to clients the valuable inverse of the bear: Expecting, loving, understanding and participating in the long-standing advances of bull markets.

James L. DiNardo offers advisory services as a representative of Northwestern Mutual Wealth Management Company (WMC), a limited purpose federal savings bank, and a wholly owned subsidiary of The Northwestern Mutual Life Insurance Company, Milwaukee, Wis., (NM). Northwestern Mutual is the fleet name for NM, its subsidiaries and affiliates. Investments held with or managed by WMC are not insured by the FDIC, are not deposits or other obligations of, or guaranteed by WMC or its affiliates and are subject to investment risks, including loss of the principal. James L. DiNardo is an insurance agent of NM (life insurance, annuities and disability income insurance), and Northwestern Long Term Care Insurance Company, a subsidiary of NM, and a registered representative of Northwestern Mutual Investment Services, LLC (NMIS), an NM subsidiary, broker-dealer, investment advisor, member FINRA, SIPC. Pioneer Financial is a marketing name used by a group of Northwestern Mutual representatives (not all of whom are affiliated with WMC) including DiNardo (referred to as the “firm”), and is not a legal entity, partnership, investment advisor, broker-dealer or affiliate of NM. The information contained in this article is not a solicitation to purchase or sell investments or securities. The views expressed herein are those of the author and may not necessarily reflect the views of Northwestern Mutual. Certified Financial Planner Board of Standards, Inc. owns the certification marks CFP®, CERTIFIED FINANCIAL PLANNER™ and federally registered CFP (with flame logo), which it awards to individuals who successfully complete initial and ongoing certification requirements.

This article was originally published in the April/May 2016 issue of Worth.